Medicare Blizzard

Medicare Is Merely An Example

Why Is Medicare Difficult?

It has not mattered who I have spoken to, where, or their backgrounds. I am on the national radio tour NOW, answering simple questions. Here are some bottom lines.

Medicare Is The Simple Example

This is NOT a flex, it is a fact. I do not sit at a computer, sharing this information with you, to prove to myself that I think I know stuff. I talk to myself all time, I don’t need to read it on my computer.

Here is why Medicare is the Simple End of the Pool

Rules known, and I have no choice other than to STRICTLY follow them.

Terminology is standardized. In life insurance, annuities, mutuals funds, ETFs, dental insurance, this is not the case, so the buyer or guidance professional is left to interpret it for you. In Medicare, the definition of services under Part A are known to every stakeholder, and you. There is not such thing as “Calculation Agent” in Medicare, as there are in your life insurance contracts.

Your access is unrestricted, and rules are in your favor, if you understand the rules.

Here is why Medicare is the Difficult End of the Pool

If the rules and language are known, why does Medicare understanding remain elusive? Here are my two cents, an incomplete list.

Start too late. I didn’t say simple rules or simple terminology. For some, the language is brand new, since your employer may have provided health insurance benefits, and only one selection. If that was the case, then you have not really needed to know too much. You do now.

Overconfidence bias by the buyer. The words may look the same, YOU THINK THEY WORK THE SAME, WHEN THEY DO NOT. You may think you understand probability better than I (which can certainly be true), but there are other commercial competitive and decision-making forces that exist, in addition to statistics. I am a very patient person when answering questions from the uninformed. I am not a very patient person when someone is wrongly implying that they have a superior set of information of factors that determines pricing of financial contracts, and then add a sense of entitlement on top of that (Imma tellin’ you, I would rather help a Medicaid recipient with negative net worth, who I can help immeasurably, as I have and will continue to do).

Fooled by Randomness (the title of my absolute #1 favorite book for everyday people to understand money). Randomness after the fact used as “evidence.” See it worked, therefore I was right. To which I respond: you may have been right this time, are you certain it wasn’t luck?1

Negative, inaccurate narratives. “It’s a trap.” This is simply untrue, it is crazy to me that I have to read this type of headline. The notion that Jae or Humana will knowingly trap you is 0%. Precisely 0%. The far more likely explanation is that you received incomplete information from someone for some reason. Keep reading.

Your Friend Isn’t Qualified To Analyze…and Neither is YouTube

Shhhh. I don’t really read the reviews of my book on Amazon.com. Guess why? In the overwhelming number of cases, the reviewer is not qualified to opine. You should not come to me for expert poker advice, I am an enthusiast. YO, this should be obvious.

I have significantly curtailed my activity on YouTube. The simple reason is that the algorithm is intentionally keeping viewers in a specific silo, but the real-world optimal solution is outside the silo. To make it worse, there are many comments that state that the silo is correct.2 So what you have:

Information isn’t complete

Non-qualified people saying that “this is the answer.”

The Worst Case Exists

The worst case is that some people with the same letters after my name are stating they are experts, but show a definite lack of knowledge of common sense, and commercial reality.3 If you look, there are dozens of videos that state or imply that Medigap Plan N is superior.

Except, videos that state that believe that Medigap Plan G isn’t worth the price have never mention the points on my Mr X spreadsheet. On top, there are hundreds of affirmation comments, including by other Medicare video-makers. That the indisputable facts in this image are never mentioned on widely-watched videos on YouTube is downright scary to me.

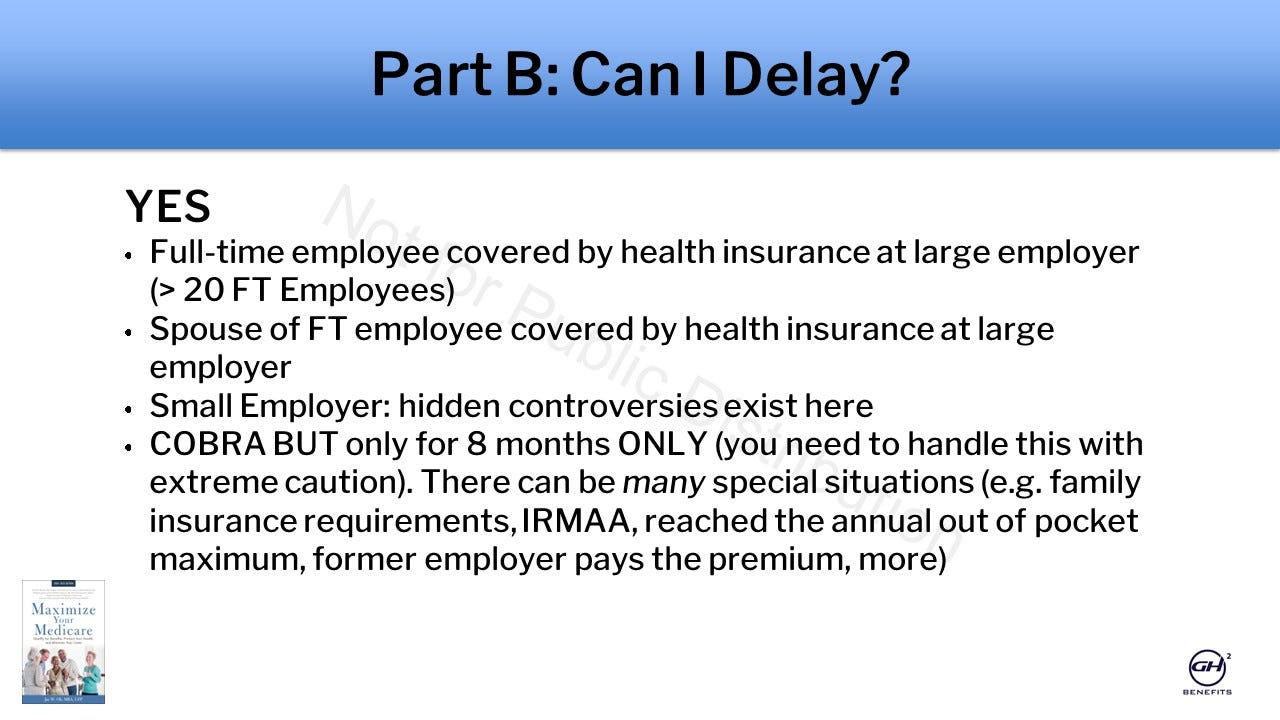

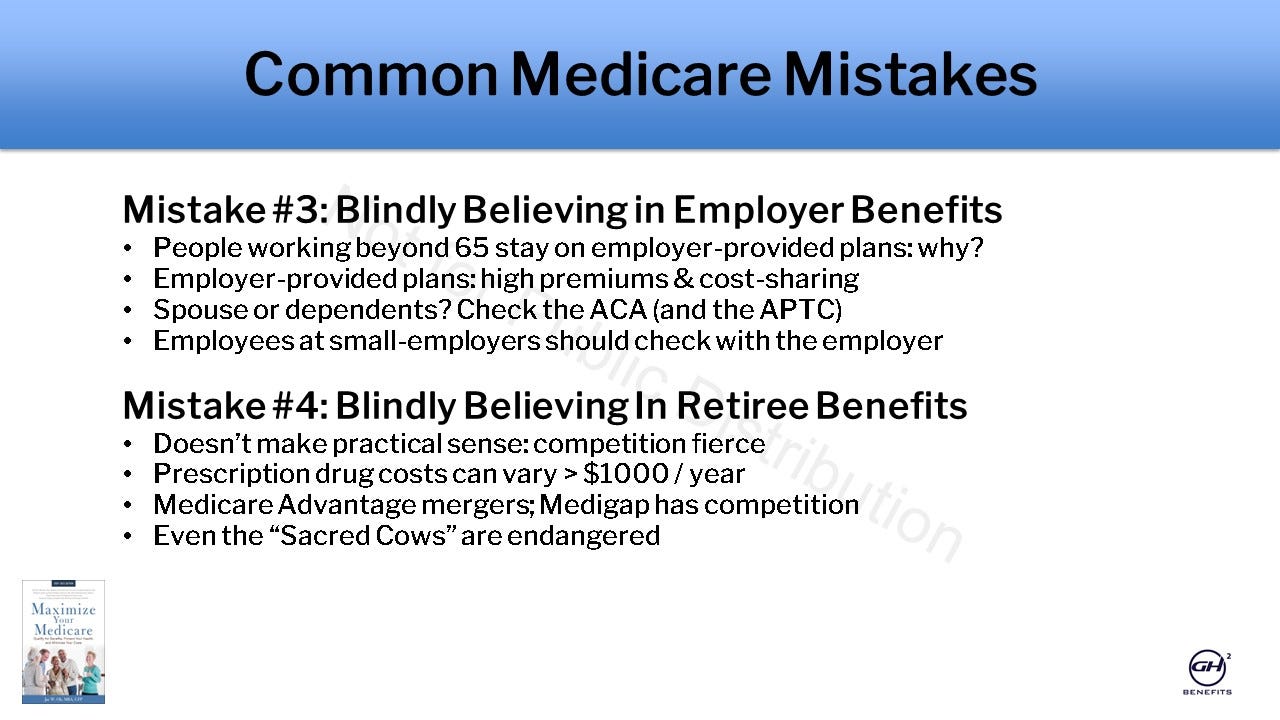

Medicare Tip: Don’t Waste Money

Yeah, I’m Captain Obvious. I promise that the combination of these two slides (part of Medicare ABCs live webinar, is being mishandled. It is resulting in:

Someone working when they want to retire, but wrongly believe they can’t.

Someone keeping a suboptimal employer-sponsored / retiree plan, when they should not.

Someone enrolling in Medicare when they didn’t need to.

Someone not enrolling in Medicare when they should have.

Easier Medicare Guidance Steps

The technology platform (which was supposed to be easy) is a pain for some to complete. Let me make it easier.

Fill this out, we will send the follow-up questions, within 24 hours (press here). You can ask whatever you want, we don’t cross the finish line until we are certain you are intentionally selecting.

The reason for the technology platform is because it is meant to help agent #3,553,236, who may or may not be fully dedicated or expert in Medicare. Here’s a secret: many “Medicare specialists” are only involved during enrollment periods. I cannot speak for them.

Your Portfolio Returns Don’t Matter, If…

Don’t forget to subscribe to Jae’s Corner on YouTube. For all my complaints about the problems created by YouTube, there is the flip side of the coin: this is YouTube’s world, I am just living in it.

Subscriber Commentary (Footnotes) Below