Top 10 Things To Check

Life Insurance. COVID has reduced life expectancy by 2 years in the US, yikes. Life insurance premiums have stayed unchanged, for the most part. For now, intense competition has kept this dynamic in place. For now. If you have not considered this, now is not a bad time to begin.

Health Insurance. If you have NEWLY purchased a marketplace plan, then you need to make the FIRST payment before 2022. This is important because otherwise, your policy will be canceled. In future months, there are grace periods, but NOT for the first payment. If you are renewing an existing plan, you don’t need to pay prior to January 1. However, you should’ve checked the premium, because your APTC may have changed, which can further reduce your health insurance premium. All ACA-compliant individual health insurance plans reset on January 1.

Medigap. Rates continue to rise, as expected, with age. If you are in very good health, you can change carriers, especially if you approaching or are over 70 years old. Technical reasons, yes. Point 1 above applies to people that are considering changing from Medicare Advantage to Medigap (that will become available on January 1, 2022).

Medigap. If you live in a state with special enrollment rights under state-specific rules, you may be able to switch carriers without underwriting. When you add this to point #3, this is a possible multi $100s/year savings.

Medicare Advantage 5-star. A larger number of plans have been rated 5-star by the CMS when compared to the past (I will have comments for paid Substack subscribers on that in the very near future). You have the annual right to change INTO a 5-star plan once a year, with no enrollment calendar. This is in effect, right now.

Taxes and your portfolio strategy. Check your non-qualified and RMDs (post-tax accounts, that is not your Roth IRA), because capital gains distributions (both long and short term) as well as RMDs are taxable. That means your individual health insurance or Medicare premiums may be affected. Last-minute moves are possible, but not if you don’t know this ripple effect exists. I promise you this is overlooked, and the effects can be enormous.

Individual Health Insurance Networks. Individual health insurance is more complicated than Medicare for the simple reason that networks here are much more fragmented than Medicare. You don’t want to be blindsided. The last result that I want for our clients is for your known healthcare providers to not accept your insurance, something that can occur.

Medicare Advantage Network. For Medicare Advantage, HMOs and HMO-POS will continue have this issue, even after the many improvements which have notably been made. Sometimes, these limitations don’t appear…until they do (Murphy’s Law is a law, after all). For those in PPOs, not to worry, in that if a healthcare provider accepts the federal Medicare card, that provider will accept your Medicare Advantage PPO.

Employee benefits. For those that are working full-time, employee benefits have continued to be added in order to address the competition for employees. For both employer and employee, short-term disability is my go-to starting point. GH2 Benefits always suggests that employers consider offering this, and always suggests that employees accept it, even if there is a cost involved. Simply put, it is the combination where price, likelihood of occurrence, and usefulness converge. If you cannot work, your rent or mortgage payment is still due, even if you refuse to go to the doctor. Enrollment periods are usually at the anniversary date of the company’s plan, so you can check. If you are a employer, competing for employees, this should be obvious.

Annuities and Long-term care. So many bells and whistles make choosing the right plan very challenging. The reason: “Joe’s Insurance Guaranteed Income Ultra” is not precisely the same as “JimBob’s Insurance Lifetime Income Plus.” The definitions of the complicated language are created by the seller, and is not regulated. That is very different than “the seller will not pay according to the language.” All of this different than a) my financial broker says they are always bad, b) my financial broker says they will always beat the returns. This is evidence of either hubris or lack of full understanding by these erroneous messages.

What You Should Do (duh)

Beat Inflation

Pure brokerage remains $0. Medicaid? Never ever a fee. Never.

But, the price of our services are certain to rise, deadline is January 15th. Existing agreements will be honored at historical rates, with our gratitude.

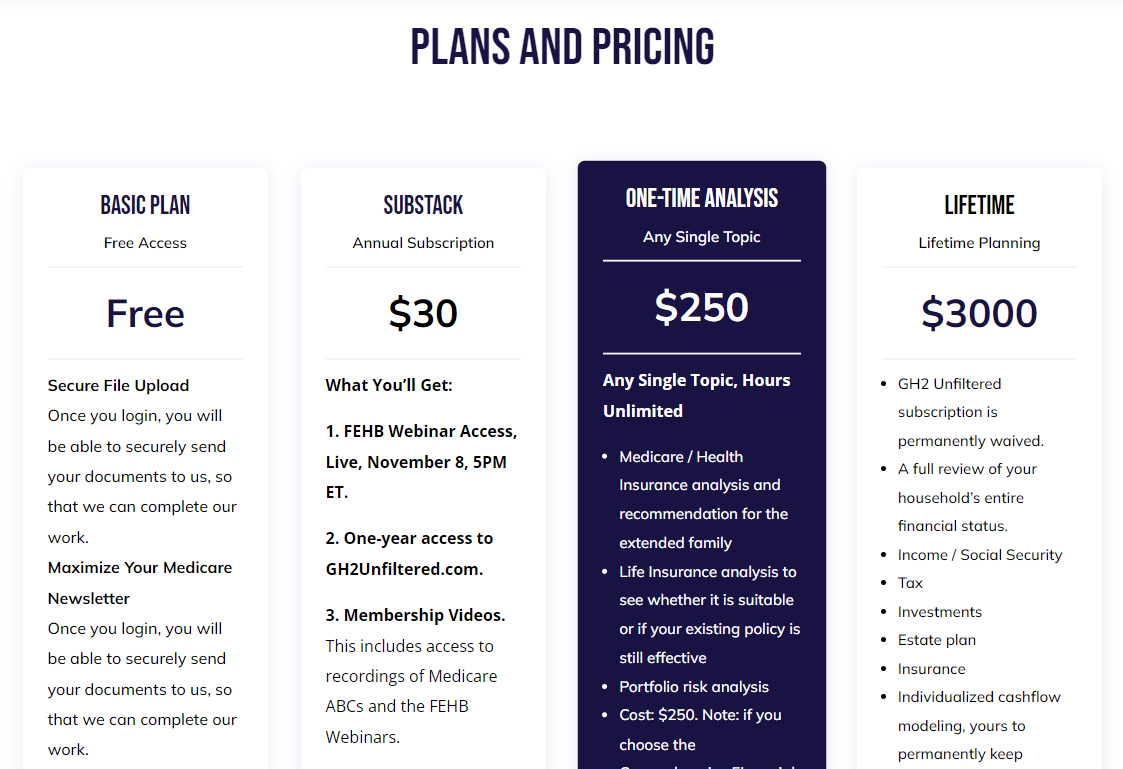

Here’s your biased hint: $3000 is a lot of money, but the new price will be higher, or completely unavailable in 2022. It is the place where your jigsaw pieces are matched with your situation and priorities, with full access to everything I know.

It takes at least 20 hours to interview you, analyze your documents, create the shared spreadsheet, and report findings so that you understand.

A very good ‘test run” is the One-Time Analysis, you’ll get a view on exactly the degree of specific information deployed in your individual instance.

Medigap Hacks

No, I am not describing myself (smirk). But, here are a few new twists and observations about Medigap from (and for) the uber-retentive (ok, now I am describing myself).