My Upcoming Article in Kiplinger's

And: Why My YouTube Channels Fail

I’ll Do Almost Anything For A Candy Bar

Here’s proof. I am pretty sure that I don’t get a full candy bar.

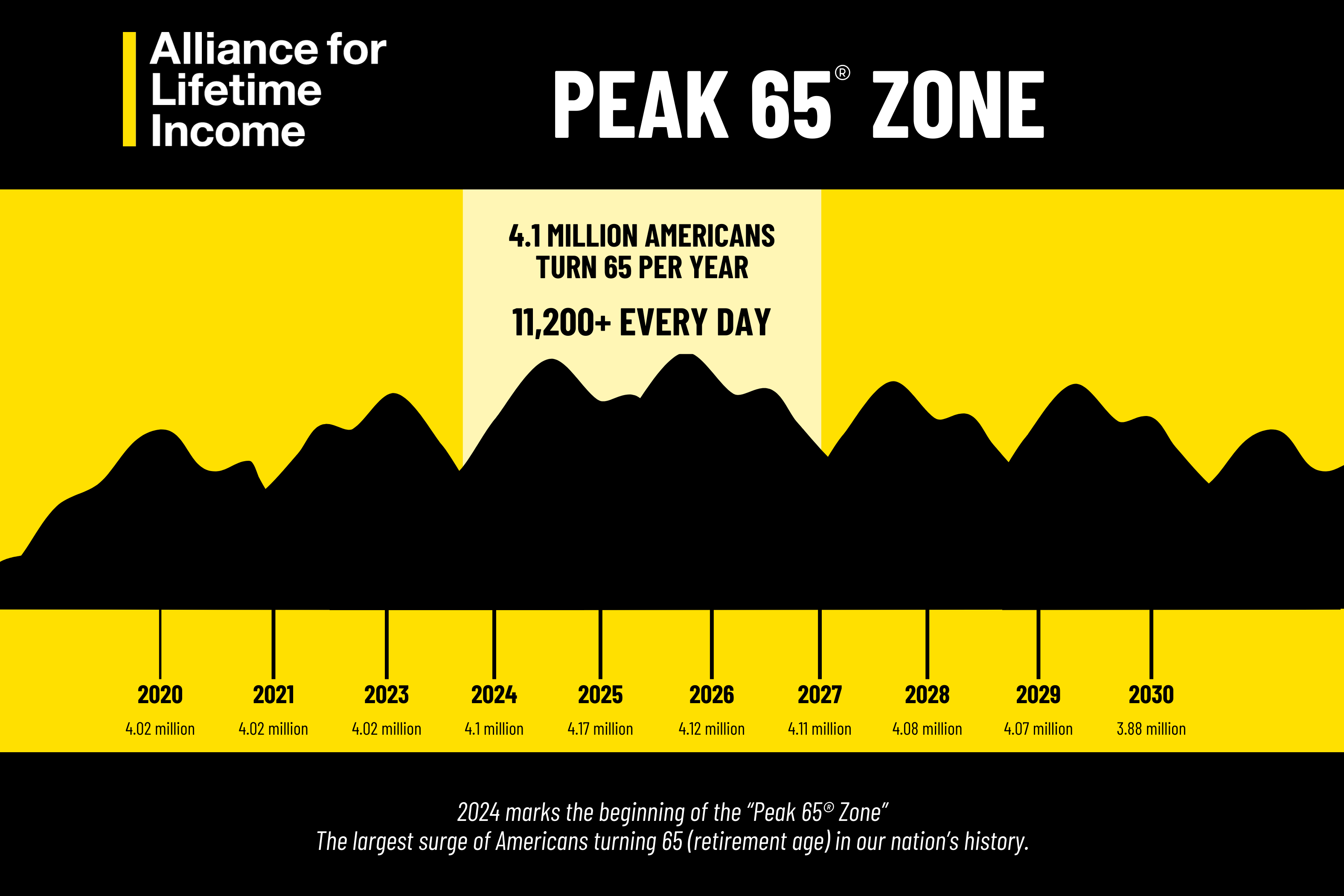

10,000 11,000 A Day Turn 65 in 2024

Yikes.

You will read that those approaching retirement are not well-prepared. There are reasons for these findings. The highest-qualified research on this can be found here, by Jason Fichtner, PhD, Executive Director at the Alliance for Lifetime Income [press here]. Disclosure: the author of Jae’s Corner is an Education Fellow at the ALI.

I am also very concerned but not necessarily for the same reasons. I am more concerned that people are not informed about how alternatives can work, how products work, to locate and execute answers.

I could start advertising the Lifetime Financial Planning Service, whose price will increase on March 1 [link]. Together, we flip over every rock, to find answers, not products.

Financial Advisory Is A Very Weird Business

When I say weird, I really mean “insufficient.” That does not mean that your advisor is a bad person. It does not mean that your insurance guy is incompetent in his stated specialty.

What do I really mean? While people need answers to solve a combination of issues, the advisory industry is focused on products. This creates gaps and holes, and they can be costly. I have tried and tried and tried to point this out.

Follow the cash flow.

If the cash flows look the same, guess what? The name of the product does not matter. It can be named a duck, it can be named an elephant. If the price of a duck is cheaper than the elephant, then you buy the duck not the elephant. This is obvious, anyone with an ounce of common sense gets it.

If you cannot re-create the elephant yourself, then fees don’t matter. If you can re-create the elephant yourself, at lower cost, don’t buy the elephant at all. Be sure that you are actually re-creating the elephant, and not the implied, non-guaranteed elephant [yes, dear Ken Fisher of Fisher Investments, I am talking to you, very specifically, and you ain’t alone].

To make it worse? The duck expert may look and sound credible, the elephant expert may look and sound credible. I do not feel pity for you, but I am empathetically stating that after a deep dive into most of the statements you read, watch or hear, errors and omissions in common sense are everywhere.

Add in behavioral bias [recency bias, availability bias, et al], and now yes, now you have a mess. Of course you do.

The point is that advisory focuses licenses, tests, certifications, etc, based on “duck” or “elephant.” The person qualified in ‘ducks’ generally is ill-equipped to have opinion or knowledge of ‘elephants.’ So you go to the 'duck store,’ and don’t get told about ‘elephants,’ for one reason or the other.

YouTube Isn’t Helping You, It’s Hurting

I largely believe that my channels on YouTube are a failure. I am almost never satisfied with my work in any way, so that is admittedly part of it. That’s my problem, not yours.

YouTube and social media is built to funnel you into continuous information about ducks, or elephants, ONLY. Every piece of advice you can read about how to be a “YouTube success” is to ‘find a niche, and try to dominate it.’ In other words, be a duck expert, or be an elephant expert.

It is not built to show you my two bullet points stated earlier. So what happens?

Only 15,000 total subscribers

Very few views, because YouTube has correctly determined that people are browsing for ducks or elephants, where my channels are focused on ANSWERS.

Maybe I should just play along. Don’t hold your breath, we will stay focused on answers.

Subscribers Get Their Advance Peek

Part of my role at the Alliance for Lifetime Income is to highlight the link between healthcare cost control and lifetime income. They are simply mirror images of one another. Lower healthcare costs = higher income, “same difference” to me. Scroll higher: answers not products.

Given Peak 65 Zone, my article in Kiplinger’s will appear soon.

For paid subscribers, a couple of things.

I literally had no idea about the length or intent of what I would write. So I proposed the full roadmap from ACA to Medicare to Long Term Care. You can see the outline that I proposed.

The draft and revisions can be followed, in advance of the publication. It is funny, I am not the only chef in the kitchen. It will be interesting to see if I am even the head chef, lol.

Paid subscribers can scroll down and click on links to access, they will be updated as we go. If you believe that you should have access, and do not, please send an email to info@gh2benefits.com. It will be corrected.